Funnel Vision #18

Digital Transformation: What does it mean for companies today?

What started as a channel for engaging customers on websites and digitizing back-end repetitive tasks, today digital is transforming not just products and processes but entire business models.

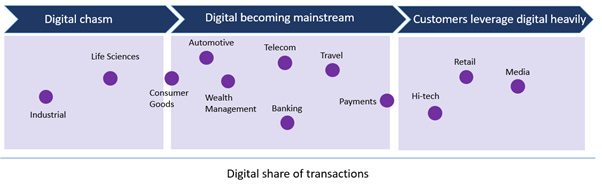

It is redefining what business companies are in, necessitating a shift in long-held organizational principles and practices and forcing renewed expectations from top management and young professionals alike. Each industry is at a different stage in the digital maturity curve yet there are common characteristics, some form of disintermediation is happening in most industries impacting value chains and business models, customer expectations are rising across the board, technology function’s role has become more pivotal, and the lines between business and technology are blurring.

Companies pour enormous resources into digital transformation programs, yet 70% of them fail. Many see sub-optimal ROI as investments in tech keep rising but results are not visible. The root cause lies in -

1. Incapable Data Infrastructure: Existing data infra created to deal with structured data is not prepared for the explosion in big data making it difficult to get to a deeper level of granularity of insights.

2. IT Processes not supporting the Agile methods of experimentation: Digital Natives have designed their systems to drive the ‘test, learn, adapt’ paradigm but in legacy enterprises, a lot of time is spent on doing the analysis first and making sure to get it correct the first time as failure might prove fatal making it difficult to drive experimentation-based improvements

3. Traditional Analytics-driven dashboards not capturing value – Aggregate views lead to a rigid approach towards analysis, limiting analytics approaches and thinking. Also, template statistical models masked as AI fail to bring out results as they lack business-specificity and do not leverage enterprises’ unique KPI tree composition.

Some specific and actionable best practices can help enterprises increase ROI -

Leveraging cloud-native architecture

Cloud Infra providers have moved on from only enabling computing facilities to providing an integrated platform as a service (PaaS). When fully integrated it standardizes technical skill sets, allows companies to predict and experiment with end-to-end customer journeys, multi-channel funnel continuity, business process throughput, marketplace dynamics and data models.

Data Lake/ Feature Store -

Engineering scalable, real-time data pipelines and integrating all data into a data lake are critical steps. These enable companies to move ahead from customer personalization to enabling automation across the ecosystem. The data strategy must include a consolidated view of structured and unstructured data types, insights from sandbox environment for developing data science, feature stores to drive cataloging and re-use of semantically consistent data, and data governance strategy driven by automation integrated into operations.

Rising expectations for a seamless experience

Customer Experience is determined by how well the brand communicates. If a customer e-mails a query and follows it up with a call, he/she expects the company representatives to be aware of the conversation history across all platforms and respond accordingly. Also, a smooth UI/ UX goes a long way in attracting and retaining customers on the platform.

Use Case: Digital Banking 2.0

Digital initiatives in banking have largely been on the transactional side, enabling customers to manage their accounts, digital payments etc. Yet the product choices available to customers are the same and customer-bank relationships have not necessarily strengthened.

FinTech firms (Neo banks, P2P Lenders, NBFCs etc.) have come up with specific products and are leveraging the right digital channels to target prospective customers. A key target for banks is to increase revenue per user- which is why cross-selling and up-selling are the top agenda of retail bankers. Banks are already taking a complete life cycle journey view of the customer and using it to offer bundled products by leveraging AI-based choice modeling to predict customer responses to create tailored offerings specific to customer micro-segments to drive maximum economic value. The focus now is on the ‘next best action’ rather than just attempting to predict the Customer Lifetime Value (CLV).

Innovations in Wholesale Banking

Many leading banks have already revamped their Operations & Technology to achieve greater delivery speed and outcomes, increase efficiency, and ensure compliance.

Ecosystem Models - The digital disruption in wholesale banking is coming not just from specialized fintech but from the ‘ecosystem’ that is emerging with Enterprise Resource Planning (ERP) Software providers at the center. Many large and mid-sized corporates use ERPs rather than proprietary bank channels to handle their payments, working capital and liquidity positions. These ERPs offering procurement, electronic invoicing, accounting or logistics support are taking advantage of their position to provide financial services directly as part of an integrated offering.

API Banking - API banking enables the bank to let 3rd part users access its custom services through dedicated APIs. The services can be spread across Accounts & Deposits, Payment Gateways, Loans and Cards, Trade Services and Business Banking etc. It is through these APIs, a business can integrate its ERP for managing its cash receivables and payables directly. RBL Bank was one of the first movers in the Indian Banking Industry to partner with 20+ partners.

Another such innovative solution is the ideation of Indian Banks’ Blockchain Infrastructure Company (IBBIC). The consortium of 18 banks aims to cut the time taken to issue domestic letters of credit from 8-9 days to 2-3 days by developing a distributed ledger (DL) system and wants to become the largest of its kind for trade finance in the country. The underlying tech ensures there are minimal documentary frauds as using fraudulent invoices or the same invoice to raise multiple rounds of financing is not possible with the DL system. Thus, minimizing the exposure of banks to credit risk and maintaining trust between merchants and banks.

With fintech startups changing the entire financial ecosystem, it becomes especially important for traditional banks to adopt digital. We are in the middle of a digital revolution, and it will surely change the way companies go about their businesses.

Meet the Author

This issue of Funnel Vision has been authored by Shantanu Chate.

Around the web in 5 stories

The Government of India announced an INR 6 lakh crore monetization plan, with an aim to improve the country’s finances. Read about it here.

API platform Postman raised $225 million at a staggering valuation of $5.6 billion to become India’s most valuable SaaS company.

Ola Electric launched its much-awaited electric scooter, with founder Bhavish Agarwal describing it as the beginning of a revolution.

The government has announced new rules for drones, making it easy for startups to do drone deliveries.

FMCG companies are adopting tech to handle their distribution systems. HUL has partnered with JioMart. There are also talks of Coca-Cola developing its own B2B e-commerce app. Interesting, isn’t it?

That’s all for this edition!

Do follow us on Instagram and LinkedIn. Stay connected for insightful articles lined up for this year.